Probability and complex function: Unit II: Two dimensional random variables

Regression

Two dimensional random variables

Regression is a mathematical measure of the average relationship between two or more variables in terms of the original limits of the data.

REGRESSION

(1)

Regression

Regression

is a mathematical measure of the average relationship between two or more

variables in terms of the original limits of the data.

(2)

Lines of regression

(1)

The line of regression of y on x is given byd eigns or ai 0 11

(2) The line of regression of x on y is given

by

Note:

Both the lines of regression passes through

(3)

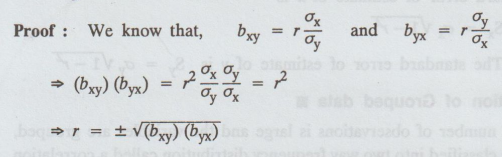

Regression coefficients

(1) Regression coefficient of y on x is r σy

/ σx = byx

(2) Regression coefficient of x on y is r σx

/ σy = bxy

Correlation

coefficient r = ± √ byx bxy

(4) Properties of Regression Lines

(1) The regression lines pass through ![]() So

So ![]() is the point of intersection of the regression lines.

is the point of intersection of the regression lines.

(2)

When r = 1, that is when there is a perfect +ve correlation or when r = -1,

that is when there is a perfect -ve correlation the equation (1) and (2)

becomes one are the same and so the regression lines coincide

(3) When r = 0 the equations of the lines are ![]() and

and ![]() which represent perpendicular lines which are parallel to the

axis.

which represent perpendicular lines which are parallel to the

axis.

(4) The slopes of the lines are r = σy /

σx , 1 σy / r σx

Since

the S.D's σx and σy are +ve, both the slopes are +ve if r

is +ve and -ve if r is -ve. That is all the three, namely the two slopes and r

are of same sign.

(5)

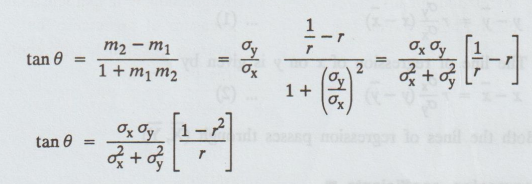

Angle between the regression lines

The

slopes of the regression lines are

m1

= r σy / σx , m2 = 1/r σy / σx

,

If

θ is the angle between the lines, then

When

will the two regression lines be (a) at right angles (b) Coincidert? [A.U N/D

2012] [A.U A/M 2019 (R13) PQT]

Note:

1. When r = 0, that is, there is no correlation between x and y.

tan

θ = ∞ (or) θ = π/2 and so the regression lines are perpendicular

2.

When r = 1 or -1, that is, when there is a perfect correlation, +ve or -ve, θ =

0 and so the lines coincide.

6.

Correlation coefficient is the geometric between the two regression

coefficients

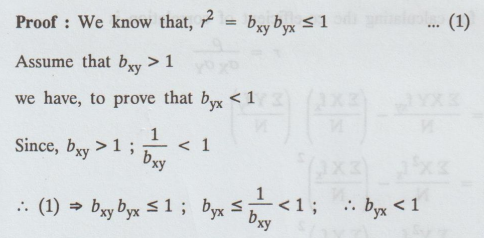

7.

If one of the regression coefficient is greater than unity the other must be

less than unity.

8.

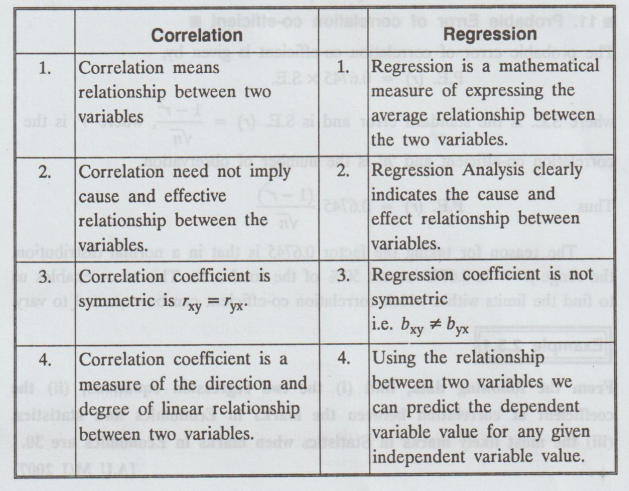

Distinguisg between correlation and regression Analysis

9.

Standard errors of estimate

The

standard error of estimate of x is

(1)

Sx = σx, √1 - r2

(2) The standard error of estimate of y is Sy

= σxy√1 − r2

10.

Correlation of Grouped data

When

the number of observations is large and the variables are grouped, the data can

be classified into two way frequency distribution called a correlation table.

If there are 'n' classes for X and 'm' classes for Y, there will be (m × n)

cells in the two-way table.

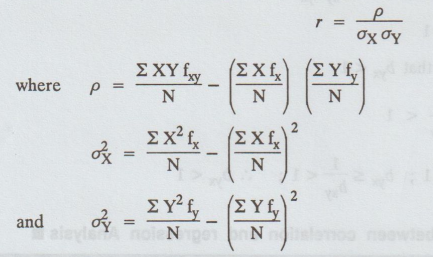

The

formula for calculating the co-efficient of correlation is

11.

Probable Error of correlation co-efficient

The

probable error of correlation co-efficient is given by,

P.E.

(r) = 0.6745 × S.E.

where

S.E. is the standard error and is S.E. (r) = 1 - r2 / √n where ‘r’ is

the correlation co-efficient and 'n' is the number of observation.

Thus

P.E. (r) = 0.6745 (1 - r2) / √n

The

reason for taking the factor 0.6745 is that in a normal distribution, the range

μ = ± 0.6745 covers 50% of the total area. This error enables us to find the

limits within which correlation co-efficient can be expected to vary.

Probability and complex function: Unit II: Two dimensional random variables : Tag: : Two dimensional random variables - Regression

Related Topics

Related Subjects

Probability and complex function

MA3303 3rd Semester EEE Dept | 2021 Regulation | 3rd Semester EEE Dept 2021 Regulation